To Buy or to Rent? Understanding The 5 Year Rule

Being a first-time home buyer in today’s real estate market can seem daunting. Besides the challenge of figuring out what you can afford, finding the right house in the right location can seem like a magic trick. With virtually no maintenance costs and the benefits of “free” amenities some apartment buildings have such as a pool, gym, and your neighbor’s wi-fi (joke), it can be tempting to stay in your rental. Renting also frees up your money for other investments (think: food truck). So what’s the point in buying a home? Let’s explore this some more.

Benefits of Buying a Home

While it may seem that renting could save you money, the truth is that your payments will never end. Rent tends to rise over time and your living situation is at the will of your landlord. On the flip side, owning a home can help grow your personal wealth. There are tax benefits (more on that later) and a lot more freedom to customize your living space.

Is Buying Always Better?

There are compelling arguments that can be made for both buying and renting. It’s enough of a conundrum that the New York Times created a detailed calculator to help people decide which approach makes sense for their lifestyle. The crucial factor in this dilemma essentially boils down to longevity — how long do you plan on living in an area?

The Five-Year Rule

There’s a rule of thumb in real estate known as The Five-Year Rule: You should keep your home for at least five years to avoid a financial loss. You’ll have a difficult time breaking even if you sell a home you just bought, even if its value has increased.The amortization schedule helps explain this concept.

Understanding the Amortization Schedule

You’ll receive a breakdown of your upcoming payments, called an amortization schedule, once you take out a mortgage on a home. It’s a table that lists each payment over the life of your mortgage and it will show you how much you’ll pay in interest each month. Let’s say you find a $400,000 home and can put 20% down. You take out a 30-year mortgage of $320,000 at a rate of 3.125%. You’d pay $173,488.52 in interest over the life of the loan, bringing your total cost after 30 years to $595,488.52. For the first eight years of your mortgage, you’ll be paying more in interest than on the principal; from the ninth year on, your interest payments will shrink as you chip away at the principal. In five years, you would have paid down $34,855 in principal, which is 8.7% of the price of the home.

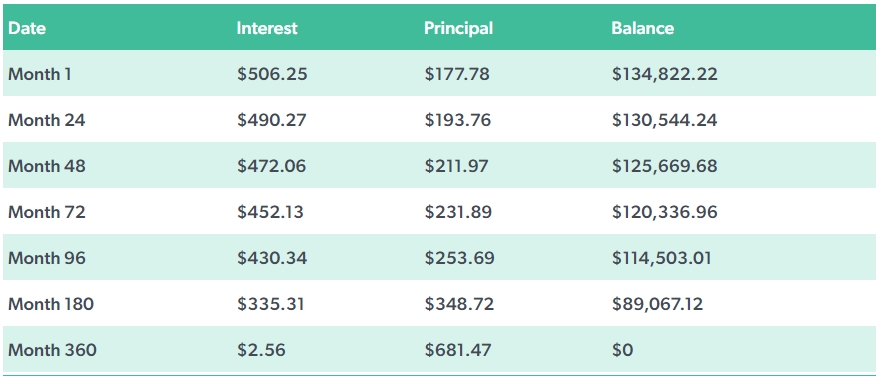

Here’s an example of an amortization schedule provided by the mortgage loan company, FreddieMac:

You bought your home for $150,000 with a down payment of 10%, resulting in a loan amount of $135,000. You secured a 30-year fixed-rate mortgage at 4.5% interest with a monthly mortgage payment of $684.03. If you stayed in your home for 30 years, you would pay $111,249.00 in interest alone over the life of the loan. To illustrate the power of interest rates, on this same loan with a 7% interest rate, you would pay $323,337 in total principal and interest. Credit: FreddieMac

Accrued Equity

Interest is heavily weighted toward the first several years of your mortgage, so it’s generally not advisable to sell a home after only a few years. Basically, the longer you stay put, the more favorable your position becomes. For example, in five years of homeownership you’ve been making payments on something that you’re on track to own; you’re not paying rent, you’re building equity. Your equity is the portion of your home that you own outright — it’s the difference between the home’s market value and what you owe your mortgage lender. Paying your mortgage steadily over the years builds equity, as does any appreciation in your home’s value (property typically appreciates at a rate of 3% every year).

What if the Value of My Home Goes Down?

There are no guarantees in any financial investment. While owning a property is generally an effective wealth-building strategy, the reality is that the value of your home can decrease. Changes to your neighborhood, such as the relocation of a major employer or a sudden housing development boom, may cause home prices to decrease. However, even if the market goes down and you lose money, the amount you would lose is less than you would lose if you were renting. For example, if your rent was $2,000 a month for five years, the value of your home would have to decrease by $120,000 over five years (less the interest you paid on your mortgage) in order for renting to be less costly than buying.

Tax Breaks and Other Benefits of Home Ownership

If you’re planning on staying put for at least five years, there’s another perk of home ownership you ought to consider: tax benefits. If itemizing deductions on your taxes makes financial sense to you as a homeowner (some people are better off taking the standard deduction rather than itemizing) you can take advantage of the mortgage interest deduction, which lets you deduct the interest you pay on your mortgage debt. You can also deduct your property taxes, and there are a number of other potential tax breaks available as well. When you eventually sell the home, the first $250,000 in capital gain is tax-free if you’re single and if you’re married, there’s a $500,000 exemption.

The choice between renting or purchasing your first home isn’t always clear, but if you have reasons to stay in an area for the foreseeable future, it’s hard to argue against ownership. If you’re looking for a home in Newport, we’ll make sure your big decision is the smartest one you can make. Reach out to me at (401) 848 – 4358 or matt@hoganri.com.

ABOUT HOGAN ASSOCIATES

Hogan Associates is an independent Rhode Island brokerage founded by Leslie Hogan and Matt Hadfield, two of Rhode Island’s most experienced agents, each with a strong track record of success in the Greater Newport real estate market. Hogan Associates’ 36 sales agents work on behalf of buyers and sellers of fine properties in the coastal communities of southern RI. The firm has offices in Newport and Middletown and is a member of Who’s Who in Luxury Real Estate, an elite broker network with more than 130,000 sales professionals located in approximately 880 offices in 70 countries and territories. In 2020 & 2021 Hogan Associates received Newport Life Magazine’s Best of Newport County award. For more information, visit HoganRI.com.